A few weeks back, we released a report on the shaky economic fundamentals of Ambre Energy’s Morrow Pacific coal export project. In a nutshell, documents released by Ambre Energy, the project’s developer, make the project look like a dud. By handling coal at two separate port terminals, Morrow Pacific incurs higher costs for transportation, operations, and capital than its likely competitors. In fact, the costs are so high that it’s not clear that Ambre could make any profit whatsoever selling coal into Asian markets.

But apparently we’re not the only ones saying that Morrow Pacific’s finances are dicey. The project’s chief executive is saying the exact same thing. A recent story in Platts Coal Trader, a subscription-only industry journal, quoted Ambre Energy’s North American CEO admitting that the project can’t make money unless international coal prices rise substantially:

A few months ago we reported on the shaky finances of Ambre Energy, Ltd, the Australian firm that’s at the center of two of the three remaining coal export terminal proposals in Washington and Oregon. Ambre’s finances paint the picture of a struggling, high-risk start-up: by the end of 2012 the company had burned through well over a hundred million dollars of its investors’ money, accumulating massive debts and obligations in the process, yet still hadn’t cobbled together even a hint of a profitable business.

But if the company’s recent financial disclosures are accurate, our earlier report just scratched at the surface of Ambre’s financial woes. Our brand-new look at the finances of Ambre’s Morrow Pacific coal export project suggests that one of the company’s export proposals is in deep financial trouble, because it faces:

Higher transportation costs than any nearby competitor;

Higher handling costs than existing coal terminal projects in the region; and

Greater capital costs than comparable export terminal projects.

Here’s another reason that coal companies have to worry about their long-term financial prospects: they’ll have to keep digging deeper and deeper to get at their coal. And digging deeper means spending more to get coal out of the ground, which can simultaneously raise coal prices and crimp coal company profits.

Even in the Powder River Basin (PRB) of Wyoming and Montana—an area renowned for its inexpensive coal—industry analysts expect production costs to rise steadily over the next few decades. See, for example, this detailed report prepared by the John T. Boyd Company, which projects steady cost increases in every single PRB coal mine currently in production or under consideration.

We’ve summarized that report’s mining cost projections in two different charts: a fancy version and a simple version. First the fancy:

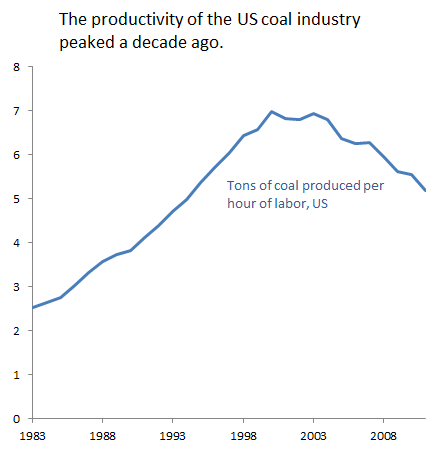

Interesting factoid: an hour of labor produces about 25 percent less coal today than it did a decade ago.

Source: US Energy Information Administration

Declining labor productivity means rising costs and slimmer profits for coal companies—adding to the woes of an industry that’s already reeling from slumping demand. But it’s not like the coal industry is doing something wrong to make productivity fall. It’s mostly a matter of geology: like any industry, coal miners started on the easy stuff—the coal that was closest to the surface and easiest to mine. But as the easy coal gets mined out, it gets harder and harder to get new coal out of the ground.

That’s the picture for the US as a whole—but the national picture includes the high-cost mines in Appalachia. So what about the western US with its cost-efficient (though environmentally troubling) strip mines?

Same basic story. Here’s a chart of the productivity of the nation’s highest-volume coal mine, the Black Thunder operation in Wyoming.

Gard Communications, the public relations firm that speaks for Ambre Energy, released a response to our report on Ambre’s finances on Wednesday. Or should I say “pre-sponse.” You see, according to the information (the “metadata“) in the computer file that Gard distributed, their “pre-buttal” was last edited on Wednesday at 9:33 a.m.—but we didn’t publish the report on our website until 10:24 that morning. Which either means that Gard got hold of a leaked copy of our report in advance (unlikely!), or else they were writing blind, complaining about “bias” in something they hadn’t actually read.

Regardless, Gard made six specific, substantive points about Ambre, designed to present its client as a stable and financially secure business. Had they read the report, they would have seen that five of the six claims were discussed in the report; the sixth was discussed at our press conference. And when considered in detail, none of the points that Gard raised put Ambre in a particularly favorable light.

So I’m actually happy that Gard has given us reason to address, in greater detail, each point they raised about their client, Ambre Energy.

1. [Ambre] has 10-year contracts to supply up to 5 million tons of coal per year to two Korean power generating companies, Korea South-East Power and Korea Southern Power.

As discussed in our report, Ambre’s FY 2012 financial report states that they have secured “10-year coal supply agreements” with the two Korean power companies. Let’s sidestep the question, for a moment, of whether using publicly-owned coal to turn the US into a resource colony for Korea is a sound long-term economic development strategy. Instead, let’s focus on the meat of those agreements with the Korean utilities.

As domestic demand for coal has tumbled, the coal industry has grown increasingly desperate to shore up falling revenues by exporting coal to Asia. And that’s why there have been so many controversial proposals to develop coal export terminals in the Pacific Northwest: the industry thinks that the Northwest offers the cheapest route to move coal from Montana and Wyoming to China, Korea, and Taiwan.

One company, the Australian-based Ambre Energy, Ltd., has put itself in the center of the coal export brouhaha by launching plans to build two major coal export terminal projects on the Columbia River. The larger of the proposed terminal projects, at a brownfield site in Longview, WA, would handle up to 44 million tons of coal per year. The smaller project, proposed to ship coal by rail to Oregon’s Port of Morrow and then barge it downstream to ocean-going vessels at Port Westward, would handle up to 8 million tons of coal annually. Both projects face major permitting, regulatory, and financing hurdles before they can get off the ground, let alone turn a profit.

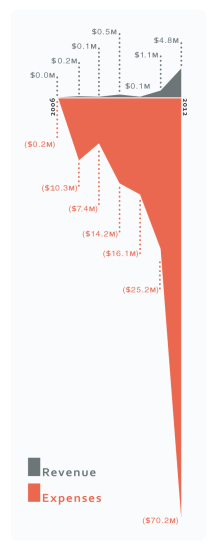

Ambre has racked up minimal revenues and massive expenses.

But while some of the other players in the coal export game are relatively well known, there’s surprisingly little reliable information in circulation in the Northwest about Ambre Energy. The company’s history, its track record, and its finances remain something of a mystery to the businesses and communities that would be affected by their coal export proposals, and to decision-makers who are deciding how to navigate the controversy. Because there’s so little information about the company out there, many people in the Northwest assume that Ambre is a major international coal company with a significant track record in the global energy industry.

But we just completed an in-depth review of Ambre’s finances, and found a story of a company with no track record of success, deeply troubled finances, minuscule overseas assets, and just over one years’ worth of experience in the US coal industry.

The chart to the right is pretty self-explanatory: the company has racked up massive expenses over the last seven fiscal years, with minimal revenues.

In short, Ambre’s finances paint a picture of a high-risk startup, rather than a stable and reliable business. The company has been losing money on risky energy investments in the US and Australia since 2005. And it didn’t even start producing coal commercially anywhere in the world until late 2011, when it bought an under-performing mining business from a US company angling to get out of the coal industry. Ambre has never come anywhere close to earning a profit, and instead has racked up massive losses for its investors—including $65 million in 2012 alone.

A few weeks ago I wrote about the astonishing and unprecedented nosedive in domestic demand for coal. That collapse has been good news for the climate and human health. But it’s been terrible, horrible, no good, very bad news for Big Coal.

And the financial markets are certainly noticing the same trends we are. Stock prices for major domestic coal companies went into a nose dive just over a year ago, and have dipped even lower this year. See, for example, this chart from Yahoo Finance:

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognizing you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

3rd Party Cookies

This website uses Google Analytics to collect anonymous information such as the number of visitors to the site, and the most popular pages.

Keeping this cookie enabled helps us to improve our website.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Additional Cookies

This website uses social media to collect anonymous information such as which platform are our users coming from.

Keeping this cookie enabled helps us better reach our audiences.

Please enable Strictly Necessary Cookies first so that we can save your preferences!

A few months ago we reported on the shaky finances of Ambre Energy, Ltd, the Australian firm that’s at the center of two of the three remaining coal export terminal proposals in Washington and Oregon. Ambre’s finances paint the picture of a struggling, high-risk start-up: by the end of 2012 the company had burned through well over a hundred million dollars of its investors’ money, accumulating massive debts and obligations in the process, yet still hadn’t cobbled together even a hint of a profitable business.

A few months ago we reported on the shaky finances of Ambre Energy, Ltd, the Australian firm that’s at the center of two of the three remaining coal export terminal proposals in Washington and Oregon. Ambre’s finances paint the picture of a struggling, high-risk start-up: by the end of 2012 the company had burned through well over a hundred million dollars of its investors’ money, accumulating massive debts and obligations in the process, yet still hadn’t cobbled together even a hint of a profitable business.