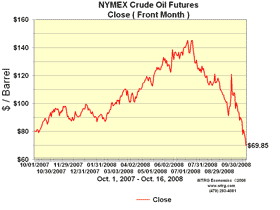

This trend may not be fully reflected at the gas pump yet, but the cost of oil is plummeting right along with the stock market. Starting in mid-summer oil prices slumped a bit, then slumped some more…and then regained a bit of ground. But just about when the economic news started looking especially dismal, the price of oil cratered—falling from over $120 to under $70 in less than a month. (The chart is courtesy of the ever-helpful wtrg.com.)

Uber-blogger Kevin Drum thinks we may be witnessing the deflation of an oil price bubble—a bubble that, like the real estate market, was fueled more by speculation than by the fundamentals of supply and demand.

Uber-blogger Kevin Drum thinks we may be witnessing the deflation of an oil price bubble—a bubble that, like the real estate market, was fueled more by speculation than by the fundamentals of supply and demand.

I think it’s a legitimate theory. When prices were at their peak, speculation in the oil markets really was far more common than people realized. Investors, rather than refiners and manufacturers with a genuine need to purchase oil, held over four-fifths of all oil futures contracts earlier this year. As prospects in housing and finance dimmed, some investors probably saw green in “black gold” (Ok, that was weird) and pumped some money into commodity markets—pushing up prices to unnatural heights.

Still, I don’t think that speculation is the whole story. Market fundamentals played a role too—creating price volatility that’s as much a problem for consumers as for energy companies.

Like just about any commodity, oil prices are set at the margins—prices aren’t set by what the average buyer thinks they should pay, but by what a few buyers are willing to pay to ensure that they get enough oil. When petroleum supplies run even a little bit tight, there are always a few buyers who are willing to pay top dollar to get enough crude. That’s why even small shortfalls in energy supplies can trigger major price increases.

Economists call it price inelasticity: over the short term, it takes a lot of upward pressure from prices to bend demand downward—oil’s such valuable stuff, there’s always someone who’s willing to pay a lot for it.

But as we’ve argued for years, oil consumption isn’t completely inelastic, especially over the long haul. Drivers have been responding to steadily rising prices with some pretty significant cutbacks in consumption—taking transit more often, driving more slowly, abandoning trucks for sedans, flocking to hybrids and high-mileage vehicles, and just generally driving less. And meanwhile, high prices have stimulated some short-term investments in increasing oil supplies.

Between falling demand and strong price incentives for oil companies to sell oil, prices started to moderate in mid-summer, as it was clear that supplies wouldn’t be as tight as some had feared. Then, the unavoidable signs of a faltering economy made further slowdowns in industrial and consumer demand—and, a further easing of any supply crunch—a near certainty.

So sure, commodity speculation may have been part of the cause of the price runup; but the collapse in prices seems to have been as much the result of actual reductions in demand as the bursting of a speculative bubble.

Regardless of the actual dynamics, though, lessons abound in the recent price collapse.

First, we simply can’t count on high energy prices or supply shortages to “save” us from climate change—at least, not on a time scale that matters. Oil markets (like all markets) are likely remain bumpy for a while, and we simply don’t know what the longer term trends will look like. I still think we could see price increases—but at this point, who can really tell? Regardless of what prices do, a smart response right now is to press even harder for policies that can guarantee long-term reductions in climate-warming emissions; we simply can’t hope or pretend that higher prices or dwindling oil supplies will do the trick on their own.

Second, volatile prices create financial risks for all sorts of energy projects—renewable and fossil fuels alike. High prices pushed a bunch of oil and gas companies into some risky ventures—the environmentally destructive tar sands in Alberta are one example. If crude prices continue to fall, some of those projects could take quite a while to pencil out—investors may find the rewards weren’t worth the risk. But the same is true for, say, some renewable energy projects: some projects that seemed like good bets when oil and gas were in the stratosphere may not work when they’re in the tank. Just so for businesses and families that invested in energy efficiency—with prices going down, it could take a while longer for some efficiency investments to pay for themselves.

So, weirdly enough, there are big sections of the energy economy—both among consumers and producers—that are hurt as much by energy price volatility as by high prices. At this stage, policies that can stabilize energy prices, wean us from fossil fuels, and encourage efficiency and renewables, will wind up benefiting energy investors, as well as home and business owners, every bit as much as they benefit the planet. (Carbon caps, anyone?)

Barry

Excellent summary. I agree that “greed” speculation only played a partial role. Also speculation isn’t just about greed. It is about what is projected to happen to demand in the future. In the summer, the world economies looked hot and so demand projection was high. Now it looks like global recession or worse so demand projections are low. This aspect of speculation is rational, reasonable and helpful to markets.You have an excellent point about volatility being a huge threat to many industries. There is an excellent long article about how this volatility has hurt American industries of all kinds in recent NYTimes Magazine. Add to your list auto-industry. They have no certainty about what products to design and tool up for. Any industry with long product cycles that are fossil fuel price dependent are getting hammered.One solution many economists, politicians and enviros are looking at recently is a “carbon tax floor”. The idea is a guaranteed floor on the price of carbon fuels. One that rises each year. This gives certainty to industry and consumers that prices will go up. If the marketplace drives the price higher, the carbon tax stops. If marketplace drives it lower the carbon tax kicks in. This is exactly the kind of carbon tax that i think we need as a society. It gives certainty to all industries about level of down-price volatility. It disappears when overly burdensome to meet goals.Sure cap is great too. But carbon taxes have some real advantages in being very quick to implement, simple to administer, less likely to be hampered by complicated exceptions and gaming. Let’s have both. Carbon tax now until effective carbon cap makes it unnecessary

sf

One thing to keep in mind is that a lot of speculators were betting that Israel was going to attack Iran, which would have resulted in a substantial proportion of the world’s oil exports being shut down for a period of weeks to months, resulting in very severe shortages. There were missile tests by Iran and war games by Israel. However, an apparent thaw in US-Iranian relations was reported by Haaretz in late spring, which claimed that the Bush administration was signaling that it did not want an Israeli attack by sending a representative to nuclear negotiations and attempting to establish an office of US interests in Baghdad. This preceded the decline in oil prices.

Alan Durning

Barry,Our point exactly re: BOTH cap and tax. (See our Cap and Trade 101 primer!)Unfortunately, carbon tax politics in Canada aren’t encouraging for spread of such a policy. I’ve got a post on the subject that we’ll publish soon.