Cascadia’s northernmost major city, Vancouver, BC, has emerged as an international poster child for home prices driven sky-high by affluent foreign buyers. Today in Seattle many fear the same scenario. Yet a review of the evidence reveals the poster version of Vancouver’s housing story is too simple, and it hardly applies at all to Seattle. And unfortunately, hyping the myth of foreign speculators distracts public debate from the more fundamental problem afflicting both cities, as well as other booming metros across North America: a shortage of homes.

In response to public outcry over housing prices increasingly out of reach to average Vancouverites, last summer British Columbia imposed a 15 percent tax on homes bought by foreigners. This year the city of Vancouver followed up with a 1 percent tax on second homes kept vacant for more than six months per year. The impact of these measures is not yet clear—the price dip that came on the heels of the foreign buyer tax was apparently temporary. Meanwhile in Seattle, although evidence is lacking, foreign investment has already been played up to the point where it has become a campaign issue in the mayor’s race, and some 2,700 people have signed an online petition for a tax.

In this article, I unpack the story of foreign investment in housing and its role in the affordability crunch afflicting people in Vancouver and Seattle. In Vancouver, evidence indicates that foreigners purchasing homes are partially responsible for a home price bubble, but that empty homes are not a major contributing factor. Vancouver’s prices are also being inflated by both a housing shortage and the self-reinforcing nature of bubbles. In contrast, in Seattle a strong local economy and limited supply of homes explains rising prices, and there is no evidence that foreign buying has played anything more than a bit part. In cases such as Vancouver, taxes intended to chill foreign demand may help some in the short term at best, but over the long term, the best solution for ending speculation is to build enough new homes.

What does foreign investment in housing look like?

Foreign investment in real estate is nothing new. In the 1980s, Japanese investors made headlines for snapping up US real estate. Historically, Canada has typically been the largest foreign investor in US real estate, though China has now claimed that spot. In recent years housing advocates have become increasingly concerned about the “financialization of housing”—excess global capital flowing into real estate in superstar “gateway cities” such as New York and London, pouring gasoline on the fire of their already expensive local housing markets.

If anything, foreign acquisition of apartment buildings is likely to help cities that need more housing, because increased investor demand boosts the incentive to build.

Foreign investment in housing comes in two main types: (1) home purchases by wealthy individuals and (2) foreign institutions investing in relatively large and expensive multi-family buildings. Here’s the important difference: the former may have a big impact on housing price inflation, while the latter does not.

In terms of rent, it matters little who owns an apartment building, because rents are primarily determined by what the market will bear. As long as a foreign institutional owner is renting out apartments just like any other local owner and not purposely keeping units vacant, the foreign investment has no effect on a city’s rents. In fact, if anything, foreign acquisition of apartment buildings is likely to help cities that need more housing, because increased investor demand boosts the incentive to build.

Some critics of foreign ownership contend that owners from abroad may be more inclined to raise rents in lockstep with what the market will bear, while small-time, local owners may let their rents lag the market, benefiting tenants. But this different landlord behavior is not determined by foreign versus local ownership but by institutional versus personal ownership. Some individual, part-time property managers do not extract the highest rents possible; virtually all institutional landlords do because their investors demand it.

Foreign institutions may also invest in housing construction. Because it generates new homes, this type of foreign investment helps put a damper on rising prices in cities with housing shortages. In Seattle, a prominent example of a housing project developed by foreigners—Canadians, in this case—is the 700-unit Insignia condo building, one of a handful of new large condo projects built in Seattle over the past decade. If foreign investors hadn’t built Insignia, up to 700 households would have been competing to buy homes elsewhere in Seattle.

The leading role of individual investors

People buy individual homes in foreign countries for a variety of reasons. This type of foreign investment puts upward pressure on prices because it boosts the amount of money chasing a set number of homes. And because that money is flowing in from outside the local economy it can feed a bubble, during which home prices rise faster than local incomes and put a housing cost squeeze on residents. Compounding the problem is the “pied-a-terre” scenario, in which a home is left empty part of the time, thereby shrinking the housing supply and driving up prices even more.

On the other hand, the existence of foreign home buyers helps developers secure financing to build more housing than they otherwise could have. In cities with few barriers to home construction such as Houston or Tokyo, foreign investment does no harm to housing affordability and may even ease prices if it yields additional homes that end up being occupied by locals.

Vancouver—the poster child?

In recent years Vancouver’s skyrocketing home prices have landed it near the top of international lists of unaffordable cities. The commonly accepted explanation goes like this (for details, read here and here): Vancouver’s historic connections to Asia have brought a large flow of Asian immigrants into the metro region over the past several decades. More recently, the explosive growth of China’s economy has generated a crop of wealthy Chinese nationals seeking homes in the Vancouver area. This often involves the “astronaut” scenario, where the breadwinner lives overseas and pays for a home for a spouse or other family members, such as children attending a university. Demand has been heightened by the unpredictable political climate in China, as many wealthy Chinese see these homes as a safe place to park their wealth. In sum, Vancouver has become a so-called “hedge city,” its home prices blown off the charts by speculative purchases by outsiders, who, to make things even more egregious, often leave their homes sitting empty.

What does the best available evidence say about all this? Is Seattle in jeopardy of the same fate as Vancouver? Read on.

What is the potential impact of foreign buyers on home prices?

Researchers from the University of British Columbia and New York University recently published an analysis of “out-of-town” home buyers. They assumed the worst case in terms of upward pressure on prices: the pied-a-terre scenario in which the homes are left empty. They applied their economic model to Manhattan, one of the world’s most attractive locations for foreign investment, where from 2004 to 2016 the (multi-year averaged) share of home purchases by out-of-town buyers increased from 9.6 to 13.6 percent. Their model predicted that the observed rise in out-of-town buying would boost house prices by 1.1 percent and rents by 1.6 percent.

While these modeling results should be interpreted with caution, the numbers do give a sense of the magnitude of price inflation caused by foreign buyers we might expect in other cities. Strikingly, the estimated impact on housing costs in Manhattan is a small fraction of Vancouver’s recent double-digit annual home price gains.

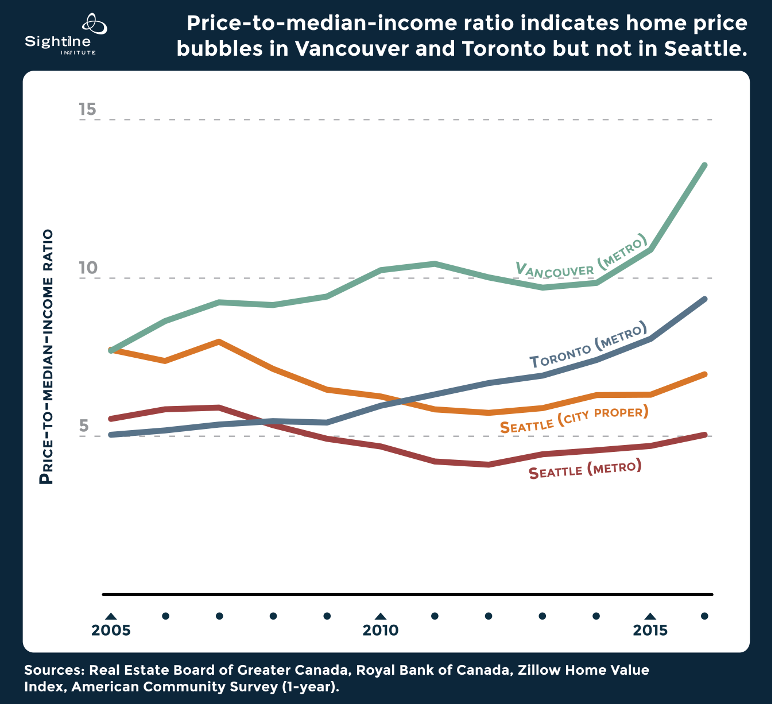

Price-to-income ratio

The relationship between incomes and home prices offers the most straightforward evidence that a housing market has gone out of whack. When prices rise faster than local incomes, either residents are spending a larger-than-normal portion of their incomes on homes, or else money is flowing into home purchases from outside the region. Either way, home prices are being driven up by something other than rising local prosperity.

And sure enough, in the Vancouver metro region, the ratio of home prices to median incomes has risen to historic highs in recent years, as shown in the graph below. Ratios around six are typical for normal housing markets in both Canada and the United States. In Vancouver, that ratio spiked to nearly 14, leaving little doubt that something unusual is happening in Vancouver. Toronto metro region seems to be on a similar trajectory, albeit not as severe.

In contrast, the data for Seattle tell a different story. For both the Seattle metro region and the city proper, after peaking during the housing bubble in 2007, the price-to-median-income ratio declined through 2012. Since then it has increased again and appears to be on an upward trend, but still remains well below the 2007 peak. Even though prices have spiraled up, the median income has kept pace fairly well, so far. Seattle’s home prices are rising fast in 2017, so the price-to-median-income trend will likely continue upward. Currently a severe lack of inventory is adding heat to Seattle sale prices, as the few homes that come on the market inevitably set off bidding wars won by the “marginal buyer” (a.k.a. the buyer willing and able to pay top dollar).

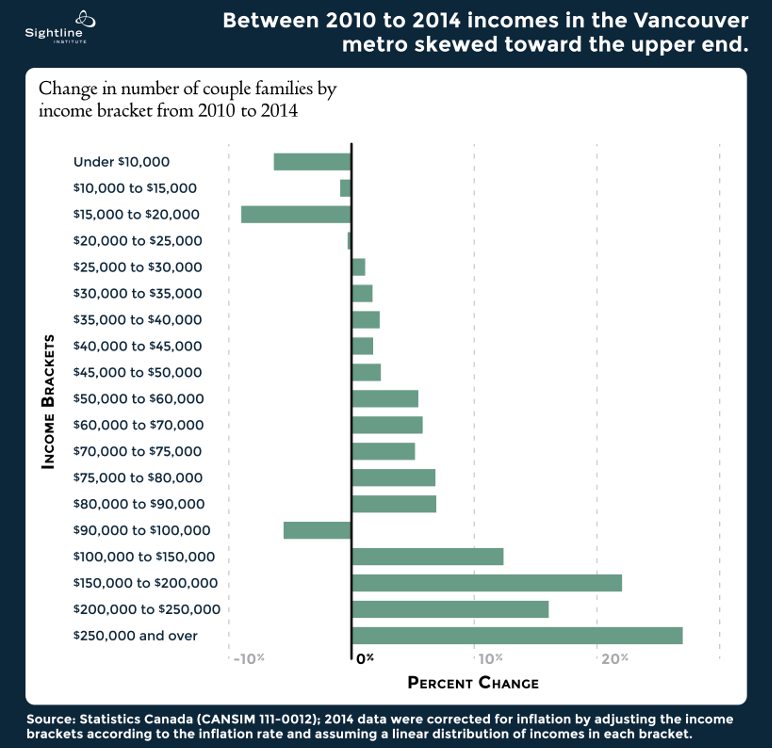

However, looking only at median income may obscure the effects of widening income inequality on home prices. In Vancouver, incomes have grown most rapidly at the upper rungs of the ladder—gains that the median may not reflect. The chart below illustrates the bulge in higher income brackets in the Vancouver metro between 2010 and 2014 (the most recent available data). Over the same time period, Vancouver’s per capita income—likely a more accurate representation of a region’s home purchasing power than the median—rose 23 percent, while median household income rose only 13 percent, signaling that the skew to upper incomes is in fact masked by the median. Furthermore, none of these income data include non-taxable capital gains such as the sale of a principal residence, which would likely inflate the high-income bulge even more.

Income gains in the upper end of the spectrum may have significant effect on prices throughout an urban housing market, particularly when homes are in short supply. So at least part of the meteoric rise in Vancouver home prices may result from disproportionately rising incomes among the well-off—gains that the median income measure fails to pick up. This suggests that the ratio of home price to median income may overstate the magnitude of Vancouver’s housing bubble, even if it accurately reflects the housing affordability challenges confronting folks at the middle of the income ladder.

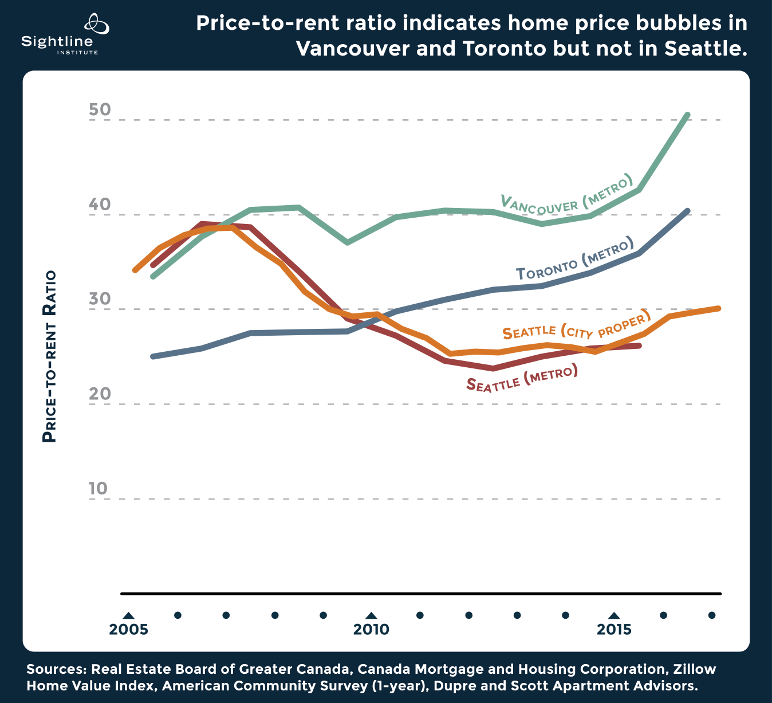

Price-to-rent ratio

A second fundamental barometer of speculative bubbles is the ratio of home prices to rents. A high ratio indicates that buyers believe a home’s value exceeds the value it can generate as a rental property. Buyers believe the price will keep rising, so they invest speculatively.

The graph above shows price-to-rent ratios for the Vancouver, Toronto, and Seattle metro regions, and also Seattle city proper. The trends are similar to the price-to-income ratios discussed previously. Data for Vancouver and Toronto indicate a growing price bubble. In Seattle the ratio his risen some in recent years but is still well below the 2006–2007 peak.

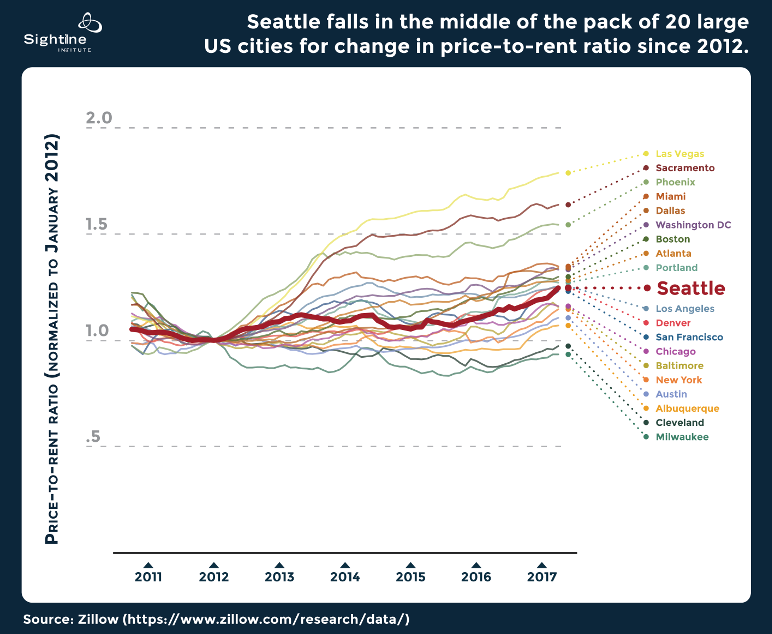

The graph below shows price-to-rent ratios in 20 large US cities, all normalized to one in 2012 to highlight how the ratios have changed since then. Seattle (the thick red line) falls in the middle of the pack, indicating nothing unusual is going on. In contrast, if foreign buyers were having a significant impact on Seattle’s housing market in recent years, one would expect to see the resultant jump in speculative value compared to rental value reflected in a steeper price-to-rent ratio climb in Seattle than in other US cities.

Are speculators buying homes and leaving them empty?

A third key factor in the foreign investment story is the extent to which speculators may be buying homes and leaving them vacant. In Vancouver, anecdotes about dark towers and half-empty neighborhoods abound, but conclusive data are hard to come by. As for rental vacancy, it’s tracked by real estate firms, and rates below 1 percent have been the norm in Vancouver over the past decade. This extremely low vacancy trend indicates that at least for the rental market, foreign investors are not buying up apartment buildings for the speculative value alone and letting them sit empty.

What about individually owned homes? The Canadian census collects vacancy data but doesn’t separate data for owned versus rented homes. Inconveniently it also lumps together multiple categories into a single metric called “non-resident occupied,” defined as a “dwelling unit that is either unoccupied or occupied solely by foreign residents and/or temporary present residents.” Further clouding the data, “unoccupied” includes not only truly vacant units in the usual sense of the word but also units that are vacant because (1) they are for sale or under renovation; (2) they are second residences, including units where students live during school; or (3) the residents happened to be away on census day.

For the City of Vancouver, the 2016 census reported a non-resident occupied unit rate of 8.2 percent, equivalent to 25,502 homes. That rate is a 6.5 percent increase over 2011 when the rate was 7.7 percent (22,169 non-resident occupied units). A much larger jump in the rate—almost 50 percent—occurred between 2001 and 2006, while from 2006 to 2011 it grew by just 3 percent. Vancouver’s Coal Harbor neighborhood stands out with a high non-resident occupied rate of 22 percent in 2016, slightly down from 2011.

A breakdown of the 2011 census data (not yet available for 2016) showed that about 4,000 of 22,000 non-resident occupied units fell into the category of foreign and/or temporary residents. The remaining 18,000 comprised 6 percent of total Vancouver homes, but as noted above, that figure includes units not truly vacant, so the actual vacancy rate was lower.

Lights off, nobody home?

For an alternate measure of vacant units, the City of Vancouver commissioned a study of electricity usage that assesses “non-occupancy” based on abnormally low power consumption. The study concluded that between 2001 and 2014 the non-occupancy rate in city of Vancouver has remained flat at just under 5 percent, and that the city rate is consistent with the rate for the entire Vancouver region. The non-occupancy rates for individual housing types were also flat over the duration of the study, with apartments hovering at around 7 percent, and single-family houses, duplexes, and rowhouses all at around 1 percent.

The census and the electricity-based occupancy rates measure different things, so we shouldn’t expect their estimates to match exactly. What’s important in assessing the potential impact on home prices is the relative change of those numbers over time. In glaring contrast, the census data show that non-resident occupied units grew by nearly half between 2001 and 2016, while the electricity-based data are flat from 2001 to 2014. This discrepancy suggests that the rise detected by the census may have been caused by increases in other sub-categories than homes that are just sitting empty for no good reason. So while there may been an increase in homes bought by foreigners, electricity data implies that most of those homes are being used.

Vacant in Seattle?

In Seattle, rental vacancy rates have remained near historic lows for the past four years, hovering at just under 5 percent. As in Vancouver, the vacancy data show no indication whatsoever that investors are buying up apartment buildings and leaving rental units empty. The best available data source for vacancy rates in Seattle’s owned homes is the census, although the ownership and rental rates are combined, and the census annual surveys have a high margin of error. The data exhibit nothing unusual in recent years. Between 2005 and 2015, the rate bounced between about 5 and 8 percent, landing at just over 5 percent in 2015.

Based on 17 years of apartment surveys, Seattle real estate analysis firm Dupre and Scott estimates that a 0.5 percent drop in vacancy rate causes about a 1 percent increase in rents. Seattle has 166,000 rental units, and last year Seattle median rent rose by 9.7 percent. For foreign-owned vacant units to have caused that rent increase, foreign investors would have had to empty out more than 8,000 previously occupied units during that single year. That is a highly unlikely scenario. And since Vancouver is similar in size to Seattle, a similarly unrealistic ballooning of vacant units would be necessary to account for Vancouver’s spiraling rents.

The Vancouver story: Putting all the pieces together

That’s like claiming there’s no shortage of tickets to see the play “Hamilton” because, even though tickets may sell for upwards of $1,000, the number of tickets sold continues to match the number of seats.

All told, Vancouver’s unusual housing market is most plausibly explained by several compounding factors that, taken together, result in too much money chasing not enough homes. Individual foreign investors are a part of the Vancouver story, but by no means the whole story. Here’s a rundown of the pieces of the puzzle:

- Price-to-median-income and price-to-rent ratios indicate a housing bubble, and foreign dollars flowing into homes explain some part of it.

- Economic modeling suggests that foreign buyers alone could not have caused such high price inflation.

- Vacancy trends indicate that homes left empty by speculators are not a major cause of the observed price increases.

- Local income has been rising faster at the high end, creating home purchasing power not reflected in the median income. In other words, the price-to-median-income ratio may overstate the size of Vancouver’s housing “bubble,” even if it accurately reflects the housing affordability problem for middle- and low-income Vancouverites.

- The bubble has snowballed as locals overextend themselves so as not to be left behind, over-exuberant flippers take big financial risks looking to make a quick buck, and parents cash in their piles of new home equity to help their kids with down payments. (In Metro Vancouver, 41 percent of owner-occupied homes are mortgage-free.)

- Lastly, evidence points to a more straightforward cause: a housing shortage driving up prices. From 2011 to 2016 metro Vancouver’s job growth of 139,000 vastly outperformed the projection of 107,500 (linearly interpolated from the 2021 projection). Meanwhile population and housing unit growth were 66,000 and 33,000 below projections, respectively. The unemployment rate is low (4.8 percent), and the job vacancy rate is high. For years Vancouver’s rental vacancy has been outlandishly low, hovering under 1 percent. (Oddly, some argue that there can’t be a shortage in Vancouver because population growth hasn’t exceeded the number of new homes built. But that’s like claiming there’s no shortage of tickets to see the play “Hamilton” because, even though tickets may sell for upwards of $1,000, the number of tickets sold continues to match the number of seats.)

UPDATE (7/11/17): Critics have correctly pointed out that this article fails to make a clear distinction between foreign buyers—that is, buyers without Canadian citizenship—and foreign capital. I focused on foreign buyers because they are the target of the two new taxes in Vancouver. Foreign capital can enter through a variety of informal channels, such as a wealthy Chinese citizen sending cash to a Vancouver resident relative who then uses those funds to purchase a home. This form of foreign capital may be a major contributor to Vancouver’s rising prices, and may even eclipse the impact of foreign buyers. But because such fund transfers are not easily tracked, it is difficult to assess the magnitude of the effect.

Should Seattle be worried?

The key metrics discussed above—price-to-income and price-to-rent ratios—indicate that Seattle is not currently in a bubble, though the data do hint at an upward trend. In short, home prices are rising fast, but on average citywide, paychecks are keeping up (while some Seattleites are falling behind, median income is still climbing). So far Seattle’s home price inflation is explained by normal economics. That’s because compared with Vancouver, Seattle has had a more sustained, hotter job market, adding many high-paying tech jobs.

When British Columbia passed its foreign buyer tax, Seattleites began to wonder if their nearby and similarly attractive city would become the next target for wealthy Chinese homebuyers and suffer Vancouver’s fate. Some local real estate agents reported an uptick in Chinese interest, and real estate web site Juwai.com saw a surge in inquiries about Seattle originating from China. Zillow, in contrast, detected no evidence of increased interest from Canada or China, and found that because Chinese shoppers target high-priced homes, they most likely only compete with highly affluent locals.

A critical difference between Vancouver and Seattle is that Vancouver has maintained stronger ties to Asia—today more than 40 percent of Vancouver metro residents have an Asian heritage. Seattle lacks the diaspora of established, concentrated Asian communities that makes the Vancouver region a desirable place for Chinese immigrants to land. With its large Asian population, the city of Bellevue to the east of Seattle may prove to be more attractive to Chinese buyers.

Last summer, the Canadian developer Burrard Group began pre-selling condos in its 374-unit NEXUS project, one of the few upcoming high-end, large-scale condo developments in Seattle. Burrard reported that the majority of buyers were “urban dwellers working in the tech industry, many of whom are renting with monthly payments that could support a mortgage,” that only a handful may have been foreign buyers, and that “there are plenty of local buyers.” Indeed, research by Zillow showed that 22 percent of Seattle renters are qualified to buy, ranking fifth of major US cities.

And while there’s gobs of local purchasing power in Seattle, there isn’t much new to purchase. Over recent years Vancouver builders have focused on condos rather than rentals, while in Seattle the opposite has been true. In 2016 alone, developers will open nearly 10,000 new apartments in Seattle. Meanwhile, over the past several years only a handful of condo projects came online, totaling perhaps 900 units (700 of which are in the Insignia building noted above). Unlike Vancouver, Seattle simply doesn’t have many new condos in which foreign speculators could park their money. And prospective foreign buyers face tough competition from Seattle’s growing pool of well-paid, condo-hungry locals.

What are the potential public policy prescriptions?

First, before rushing to enact deterrents to foreign buying, cities can get a better handle on what’s really going on, and that means more robust data on both the number of foreign purchases and the number of vacant units. British Columbia only began tracking “foreign buyer involvement in residential transactions” a year ago. The government of Ontario just released their first data set showing that foreign buyers accounted for 4.7 percent of home purchases, corroborating a January report by the Toronto Real Estate Board that also estimated that only a quarter of the foreign purchases (1.25 percent of the total) may have been speculative investments. In Melbourne, Australia, analysts assessed empty units by monitoring water usage, similar to Vancouver’s approach with electricity. If Seattle’s leaders are concerned, the time is now to start collecting data so as to avoid uninformed responses to what appears to be a negligible problem so far.

Foreign buyer tax

British Columbia’s 15 percent foreign buyer tax appeared to have a rapid, dramatic impact on home sales after it was imposed last August, but the latest data suggest that the cooling effect was temporary, with current home prices up 8.8 percent over a year ago. One local expert contends that even a 30 percent tax wouldn’t have an effect on anything but high-end homes. In March, BC lawmakers proposed tweaks to exempt those with work permits who pay income taxes and to offer a rebate to people who attain citizenship after paying the buyer tax. Spurred by spiraling prices in Toronto that some believe reflect foreign demand redirected from Vancouver, in April the province of Ontario enacted a foreign buyer tax, and Victoria, BC, is asking the provincial legislature to extend the Vancouver-area foreign buyer tax to Victoria as well.

Soon after the BC foreign buyer tax was imposed, a Chinese national subjected to the tax filed a class action lawsuit based on constitutional grounds, but the case has yet to hit the courts. In Seattle, a foreign buyer tax would face formidable legal hurdles. The most likely approach would be a real estate excise tax (REET), which cities cannot impose without authority from the State. As a gauge of the political difficulty involved, over the past two years, advocates have had little success in getting the state to authorize Seattle to impose an ordinary REET to fund affordable housing. Even if authorized, a foreign buyer tax could be susceptible to federal constitutional challenges related to either the 14th Amendment Equal Protection doctrine or right-to-travel and the Commerce Clause. Enforcement would also pose difficulties: counties, not cities, register land sales and do not currently check the nationality of buyers. Besides, there are numerous ways foreign buyers could skirt a tax by hiding status, for example by setting up a US corporation.

Vacancy tax

In November, the City of Vancouver approved a new empty homes tax that assesses an annual 1 percent tax on the value of any home occupied fewer than six months out of a year. Note that the tax was passed even though the city lacked evidence for an increase in vacant homes commensurate with the rapid home price escalation over the past few years. Homeowners must self-report to pay the tax and the first deadline is in February 2018, so the effect remains to be seen. In Seattle, an empty home tax would face even bigger legal roadblocks than would a foreign buyer REET. Such a tax would likely be interpreted as a non-uniform property tax, which is prohibited by the Washington State constitution.

Progressive property surtax

Academics in Vancouver have proposed a “progressive property surtax” intended to target foreign homeowners not contributing to the local tax base. It would impose a progressively increasing property tax on expensive homes—for example, starting at 1 percent for a $1 million house—but with an important twist: it would allow deductions for any income tax paid by the owner. Most homeowners working in the province would pay no additional tax because their income tax bill would more than cancel out the property surtax. Foreign owners not paying income tax in the province would get hit with the full property surtax, dampening the attraction of homes as speculative investments. It’s a clever idea, though irrelevant to Seattle: Washington has no income tax, and even if it did, the state constitution’s rules on uniform property tax would preclude a progressive property surtax.

Flipping tax

Hot markets incite speculative flipping—buying a home with the intention of reselling it quickly for a hefty profit—a practice that exacerbates price bubbles. Because flipping is typically more common with local buyers than foreign buyers, a flipping tax isn’t likely to chill foreign investment much, but it may be an effective tool for reining in bubbles, whatever the causes. British Columbia already has what is effectively a flipping tax: 100 percent of the profit on the sale of a home not intended as a principal residence must be counted as taxable income. Alternatively, governments could impose a special transfer tax on homes bought and sold within a given period of time—one year is a common assumption. In Seattle, such a tax would likely come in the form of a REET, which would require difficult legislative approval at the state level. A targeted capital gains tax is another as yet untried possibility.

Getting past Band-Aids

Price bubbles feed on scarcity. (Anyone standing in a line around the block to see a rental unit or getting priced out in a homebuyers’ bidding war can understand how this works). If developers could build enough homes to meet rising foreign demand, prices would cool, a bubble would be averted, and foreign buyers would be a non-issue. However, in expensive metro regions such as Vancouver and Seattle, restrictive regulations are already builders from making enough homes to meet existing demand, conditions that are like a petri dish for a home price bubble when outside cash is injected into the system.

All bubbles eventually pop, returning prices to normal and leaving hapless speculators holding the bag. Just such a reset is currently happening with high-end homes in New York City and London. Still, home price bubbles create chaotic housing insecurity that inflicts disproportionate harm on lower-income people and families. Taming bubbles clearly serves the public interest.

When there is a bubble, a foreign buyer tax that weakens demand may be justified to help cool a market spinning out of control, as in Vancouver. The psychological deflating power alone may be worth the likely unintended consequences. Same goes with an empty home tax. Even though the vacancy data and economic modeling discussed above suggest that empty homes are not a major contributor to Vancouver’s surging prices, the tax might do some good—or at least no harm. In Seattle, which appears to have neither a bubble nor excess empty homes, both taxes are largely irrelevant, not to mention legally out of reach.

The big shortcoming of these taxes is that they are Band-Aids. They don’t address the root problem of housing scarcity. What’s more, by adopting such policies, cities put themselves in the counterproductive position of no longer welcoming affluent immigrants only because there isn’t enough new housing to accommodate them. Plus, thwarted demand will just redirect to another city. Is Canada prepared to impose foreign buyer taxes throughout the country? What are the potential large-scale economic downsides of discouraging the immigration of prosperous foreigners?

The alternative to walls—that is, to anti-immigrant Band-Aids—is letting a city grow up and make room for all the people who want to live there.

Over the long term, cities sell themselves short by putting up walls to outsiders. The alternative to walls—that is, to anti-immigrant Band-Aids—is letting a city grow up and make room for all the people who want to live there while keeping prices stable for those who have long lived there. And that comes down to relaxing zoning to allow more homes on a limited amount of land and fixing onerous rules and approval processes that that needlessly make homebuilding more expensive. Seattle and Vancouver both face a particularly challenging barrier to welcoming newcomers and keeping their cities affordable for long-timers because they set aside so much of their land for single-family houses on large lots.

Some worry that foreign capital is so bottomless that no matter how much Vancouver builds it won’t be enough to make a dent in prices. Indeed, Chinese purchasing power seems unprecedented, but international economic conditions can change fast. In any case, however high the demand may be, adding new homes will always help keep prices lower than they would otherwise have been, and also makes speculative investment less enticing.

Scarcity is what makes homes attractive places to park money. People speculate in homes and art and precious metals because their supply is limited. No one speculates in ballpoint pens, because pen makers can just make more. Ultimately, the way to make foreign money a non-issue is to make the housing market more like the ballpoint pen market: easy to make more. Besides, all those new homes bring the added benefit of giving more people the opportunity to live in compact, walkable communities—good medicine for their health and for the planet, too.

Conclusion

The potential impact of foreign investment on housing affordability is a hot topic in Cascadia’s two largest cities, Vancouver, BC, and Seattle. In Vancouver, foreign buyers are no doubt fueling some of the home price inflation that exceeds local income growth. Evidence does not support laying blame on speculators leaving homes empty, but does indicate that a housing shortage is also contributing.

Assertions that Seattle’s home prices are being similarly driven up by foreign buyers are unfounded. Currently Seattle’s economic fundamentals of job and income growth explain home prices, so at most, the city should monitor foreign buying and vacancies as a precaution. Taxes on foreign buyers or empty homes may be helpful partial responses to housing bubbles, where they occur, but the surest way to end harmful speculation in the housing market is to deal with shortage by creating ample homes.

NOTES AND DATA SOURCES

Thank you to Jens von Bergmann with MountainMath for sharing suggestions, data, and the excellent Census Mapper tool.

Estimates of median household income for the Vancouver and Toronto metros were provided by the Royal Bank of Canada (Robert Hogue, private communication). Home prices for the Vancouver and Toronto metros are from the Real Estate Board of Greater Vancouver’s MLS® Home Price Index. Average rents for two-bedroom apartments for the Vancouver and Toronto metros are from the Canada Mortgage and Housing Corporation.

Home prices for the City of Seattle and the Seattle metro are from Zillow’s Home Value Index. Median income data for the City of Seattle and the Seattle metro are from the US Census American Community Survey (ACS) 1-year averages (Table S1901). Because the ACS has not yet published 2016 income data, the 2016 data points shown in the graph above are estimated based on a linear extrapolation of the observed trend between 2012 and 2015. Median contract rent for the Seattle metro is from the ACS 1-year survey (Table B25058). Median rent for apartments in 20+ unit buildings for the City of Seattle and estimated effect of vacancy rate on rent are from Dupre + Scott Apartment Advisors (Mike Scott, private communication).

Vancouver metro median income data for 2010 and 2014 are from Statistics Canada (CANSIM 111-0012). The 2014 data were corrected for 7 percent inflation from 2010 by adjusting the income brackets according to the inflation rate and assuming a linear distribution of incomes in each bracket. The Canadian census divides income data into three household types: couple families, lone-parent families, and persons not in census families. Median income for each of the three types increased by 12–13 percent from 2010 to 2014, so the couple family data shown in the bar chart are representative of all three household types. Average income for the Vancouver metro is from Statistics Canada, based on income tax returns.

In the Ecotagious study of electricity consumption, a unit was classified as non-occupied for a year if low usage data showed it was unoccupied for August, September, and the following June and July (the “non-heating” months better isolate usage associated with actual occupancy). To be deemed unoccupied for a given month, the unit had to be unoccupied for 25 or more days in that month, a cutoff intended to eliminate infrequent use of the home, such as a domestic worker coming in once a week.

As an example of how the issue of foreign investment has been so susceptible to hype, the United Nations Report of the Special Rapporteur on the “financialization of housing” includes an incorrect data point on vacancy in London that grossly exaggerates the reality. On page 10, the author writes that “in the affluent boroughs of Chelsea and Kensington in the city of London, prime locations for wealthy foreign investors, the number of vacant units increased by 40 per cent between 2013 and 2014.” However, the data source cited shows no such increase in those years. For “All Vacant Dwellings,” there was a 16 percent increase between 2011 and 2012, but in 2013 it dropped below the 2011 level and kept dropping through 2015. For “All Long-Term Vacant Dwellings,” there was a 25 percent increase between 2012 and 2013, but in 2014 it dropped right back down to just 3 percent higher than it was in 2012. Overall, the data show that the number of vacant units in Chelsea and Kensington has stayed relatively flat from 2004 to 2015.

Correction: This article originally included an incorrect statement about a US federal tax foreign sellers, and the statement has been deleted.

Comments are closed.